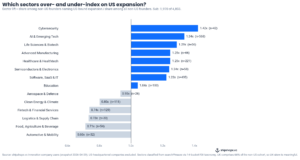

Cybersecurity founders outside the United States are forty-two per cent more likely than the average non-US founder to name the US as a target market. Automotive and mobility founders are thirty-five per cent less likely. Physical production lines are painful to move. Software and Digital Services are not.

The trans-Atlantic corridor and the trans-Pacific one, and every other corridor that ends in America — is real, but not all industries face equal hurdles. Stated intent reflects this.

Across 4,803 non-US-headquartered companies in this sample (from shipshape.vc’s innovation-company users dataset), 1,970 (forty-one per cent) name the US as an expansion destination. shipshape.vc is a free investment search engine that helps innovation companies access free research on potential investors (VC, CVC, PE).

The headline number is even across the sample as a whole, but the sector mix underneath it isn’t. Eight sectors over-index on US-bound expansion; six under-index; and the line between the two groups has structural themes rather than incidental.

Where the data comes from

This piece is built on the international expansion intentions of 4,803 non-US-headquartered companies registered on shipshape.vc as of 29 April 2026. We exclude US-headquartered companies entirely; the question we are asking is which non-US founders are pulling toward America, not which Americans are staying within their own borders.

We count a company as US-bound if it states it wants to expand to the United States. Sector tags are derived from each company’s free-text searches via a fourteen-bucket sector classifier.

Companies can be tagged with more than one sector. All percentage lifts are computed against the relevant baseline, so “Cybersecurity 1.42×” means that cybersecurity firms among US-bound non-US founders are forty-two per cent over-represented relative to the population of all non-US founders in the dataset.

The over-indexed eight: tech, and tech-enabled industrials

The eight sectors over-indexed on US expansion are cybersecurity (1.42×), AI and emerging tech (1.34×), life sciences and biotech (1.29×), advanced manufacturing (1.25×), healthcare and healthtech (1.25×), semiconductors and electronics (1.24×), software, SaaS and IT (1.22×), and education (1.04×, essentially neutral). Education aside, the cluster is coherent: it is tech, plus the parts of industrials and biosciences whose product can be knowledge work delivered through software or licensable IP.

What these sectors share, and what the under-indexed six don’t, is product portability and a clear North Star in terms of largest global market. A cybersecurity firm sells a SaaS platform to a US enterprise and ships its product over the wire. A biotech firm can license out molecules and in theory can runs trials with US partners. A semiconductor design firm sells IP cores; an AI firm sells API calls; a healthtech firm sells per-seat software to US health systems (and hardware can mix in too, and whilst there are regulatory costs here, the size of the US market is so vast). Many of the businesses in these sectors do not have needs to physically build a factory, sign a long-term lease, secure a Class-A regulatory permit, or recruit a thousand drivers in the United States to start generating American revenue. The capital required for an initial US presence can be small. Founders in these sectors look at the US and see a market they can credibly enter from a London or Dublin or Berlin desk.

The under-indexed six: physical-economy and regulated sectors

The six under-indexed sectors are: aerospace and defence (0.93×), clean energy and climate (0.80×), fintech and financial services (0.74×), logistics and supply chain (0.73×), food, agriculture and beverage (0.71×), and automotive and mobility (0.65×).

Founders in these sectors are less likely to name the US than the average non-US founder, and the under-indexing is consistent across the cluster.

What the six share is that their products typically live somewhere physical and/or regulated, and so a potential hypothesis emerges.

Auto and mobility firms need more infrastructure, regulatory relationships and sometimes a relationship with a tier-one OEM that probably doesn’t have a US plant. Clean energy firms need power-purchase agreements that look different in every US state and federal incentives that have shifted twice in three years.

Aerospace and defence firms need ITAR clearances and a primes relationship that takes years to build. Fintech firms need state-by-state licensing and a relationship with a US sponsor bank. The cost and time required to make the first dollar of American revenue, in each of these cases, is often materially higher than for a SaaS product, and the regulatory exposure is a continuous cost rather than a one-off entry fee.

The two contrarian sectors here, in different ways, are fintech and automotive.

The fintech under-indexing is interesting because the trans-Atlantic fintech corridor is one of the most-discussed corridors in the industry press; one might reasonably expect to see lifts above 1.0 rather than 0.74. The corridor narrative is partly true — there are well-known non-US fintechs that have crossed — but it is not a representative pattern in this dataset. Non-US fintech founders, in aggregate, are more likely than not to be focusing on Europe, the GCC and other markets where the regulatory architecture is more familiar than fifty separate state-level money-transmission regimes plus federal sponsor-bank relationships. The corridor exists for a small number of well-capitalised companies; for the median fintech founder in our data, it does not seem to be the path of least resistance.

The automotive and mobility under-indexing (0.65×) is the deepest in the dataset and reads, structurally, as the inverse of the most-aggressive US-state FDI activity. Michigan, Tennessee, Texas, Georgia, Ohio and Indiana have all run heavily-resourced auto-EV inbound campaigns, and yet non-US auto and mobility founders are almost a third less likely than the global non-US average to name the US as a target. This isn’t to suggest that resourcing to attract FDI in these areas is a waste, but correctly, that more effort and resource is needed.

This could be the Inflation Reduction Act creating two distinct populations: the existing global OEMs and tier-one suppliers, who are absorbing IRA-stimulated US investment opportunistically, and the early-stage non-US founders in our dataset, who see the IRA’s domestic-content rules as a barrier rather than a magnet.

What this changes for founders, advisors, and for FDI teams

For founders, the diagnostic value runs in both directions. If you are in one of the eight over-indexed sectors and you are not targeting the US, you are moving against the cohort, and the question worth asking is whether you have a specific reason that justifies it — or whether you are simply behind your peers (or pursuing an asymmetric approach). If you are in one of the six under-indexed sectors and you are targeting the US, you are moving against the cohort in the other direction, and the question worth asking is whether you have a specific structural advantage — a US partnership, a regulated product that already meets US specs, a customer who has pulled you in — or whether you are over-extending without one.

For US state FDI teams, the implication is sharper. The eight over-indexed sectors are the audience that is already pulling toward the United States; the marketing problem there is largely about which US state, not whether to come at all. The six under-indexed sectors are the audience that is, by default, not as likely planning expansion to the US; the marketing problem there is to give them a reason to overcome the structural friction at the entry point. A pitch to a UK or German cybersecurity founder is operating with the wind; a pitch to an EU auto-mobility founder is operating against it. The two campaigns of outreach, white-glove treatment and incentives are not the same campaign, and they probably be funded differently.

For policy-makers, the under-indexed cluster is a measurable lens on where US regulatory architecture is acting as inbound friction rather than inbound attractor.

Fintech, automotive, food and agriculture, clean energy, logistics — every one of these is a sector where the United States has both a large addressable market and a regulatory regime that meaningfully complicates non-US entry.

The corridor problem in each of those sectors is not lack of interest; it is lack of an entry pathway that is comparable to European or Gulf alternatives.

We will revisit this picture as the dataset grows and as the policy environment moves. The eight-up / six-down split is the kind of pattern that should be stable; the magnitudes inside each cluster — particularly the fintech and automotive under-indexing, which are the figures most exposed to specific regulatory choices — could move quickly if those choices change.

If you would like to explore the underlying data or compare it to your own pipeline, get in touch via daniel@shipshape.vc. If you would like advice on US market entry, Bill Kenney runs a US expansion consortium that has a multitude of advisors offering office hours; if you would like to participate, reach out to bill@meetroi.com.