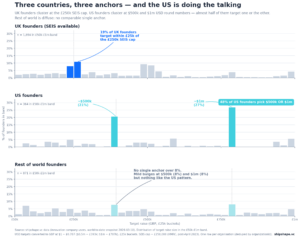

Almost half of US founders in our dataset who are targeting a raise between $50,000 and $1 million pick exactly $500,000 or exactly $1 million. The two USD round numbers between them account for 48 per cent of the US distribution in this band. UK founders, by contrast, cluster sharply at £250,000 — the SEIS cap. Founders from the rest of the world do neither: their target raises are spread thinly across the band, with no single anchor crossing 8 per cent.

When we first looked at this distribution, we drew it as UK versus non-UK and concluded that non-UK founders cluster at $500,000 and $1 million round numbers. That framing turned out to be hiding the actual story. Once you split non-UK into US and the rest of the world, the round-number anchoring is overwhelmingly an American phenomenon. The rest of the non-UK world is comparatively eclectic — they have a mild preference for the same USD round numbers, but it is nothing like the US pattern.

Where the data comes from

This piece is built on the target raise sizes of 2,929 founders who have used shipshape.vc and recorded a target raise between £50,000 and £1 million, drawn from our innovation company users dataset (snapshot 2026-03-10, world-to-date). We use one row per organisation, deduplicated by organisation ID, and bucket targets into £25,000 bins. USD-denominated targets are converted to GBP at $1 = £0.787, which puts $500,000 at roughly £394,000 and $1 million at roughly £787,000. The country split is United Kingdom (n=1,694), United States (n=364), and rest of world (n=871).

The UK anchor: a tax cap, not a number preference

Nineteen per cent of UK founders in this band target within £25,000 of the £250,000 SEIS cap. The cap is a hard policy line: an investor putting money into a SEIS-eligible round can claim 50 per cent income tax relief on up to £200,000 of investment per tax year, and the company can take a maximum of £250,000 in SEIS-qualifying investment over its lifetime. Going one pound over the £250,000 cap means none of the marginal money is SEIS-qualifying for the company. UK founders are not picking £250,000 because it is a pretty number; they are picking it because the tax architecture creates a discontinuity at exactly that point and they are trying to maximise the part of their round that sits inside it.

The US anchor: round numbers as the default vernacular

Twenty-one per cent of US founders in this band target $500,000, and 27 per cent target $1 million. Combined, 48 per cent of US founders pick one or the other of those two specific USD figures. By comparison, the next-largest single bin in the US distribution is at 6 per cent. The concentration is unusually sharp.

Our reading of this is cultural rather than structural. There is no US tax line that runs through $500,000 or $1 million the way the SEIS cap runs through £250,000. What there is, instead, is a deeply ingrained US fundraising vernacular in which “we’re raising a five hundred K round” or “we’re raising a million” is how the conversation starts. Round numbers are the default unit of trade in the language of US early-stage fundraising. Founders are not so much sizing their raise to the company’s needs as picking the closest culturally legitimate round number to the size they roughly think they need. The implication is that target raise size, for US founders, is more weakly correlated with the underlying business plan than founders in other markets might assume.

The rest of the world: anchored to nothing in particular

For founders raising outside the UK and US, the distribution is materially flatter. The single largest bin is 8 per cent at the £775,000 mark, which is the GBP equivalent of $1 million; the next-largest is 8 per cent at £375,000, the GBP equivalent of $500,000. So the USD round-number bulges are visible, but they are bulges rather than spikes, and the rest of the distribution is genuinely spread across the band. We read this as a population of founders without a single dominant anchoring convention. Some are raising in their local currencies and pick local round numbers. Some are raising in USD and inherit the American convention. Some are sizing to specific milestones and pick whatever number that produces. The aggregate is diffuse because the underlying behaviours are heterogeneous.

What this changes

For founders, the most useful read of this chart is that target raise size is one of the easier places to differentiate yourself from the median. Half of your American competitors are picking the same two numbers; if you can articulate why your target is the smallest amount that gets your business to its next defensible milestone, you are doing something most founders in your peer group are not. For UK founders, the SEIS cap is doing real work, and a target near £250,000 is harder to read as either thoughtful or thoughtless without knowing the company; the right diagnostic question is whether the cap is shaping the round size or whether the round size happens to align with the cap.

For investors, the diagnostic value runs the other way. A US founder asking for $500,000 or $1 million is, statistically, picking the cultural default. That is not necessarily wrong, but it is worth treating as a starting point for a conversation about what the company actually needs, not as evidence that any particular sizing exercise has happened. UK founders asking for figures near £250,000 are reading the tax incentive correctly; the more interesting question is what they would do if SEIS did not exist. And founders raising from the rest of the world, by virtue of having no obvious anchor to ask about, may be the cohort whose target raise size most directly reflects their business plan.

We will revisit this distribution as the dataset grows. The US round-number concentration is sharp enough that we would expect it to dilute somewhat as the sample broadens, but the underlying point — that founders in different markets are anchoring to materially different things — is unlikely to go away.