What Two Years of Expansion Data Says About the UK as a destination for innovation companies

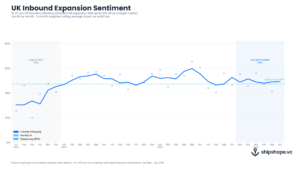

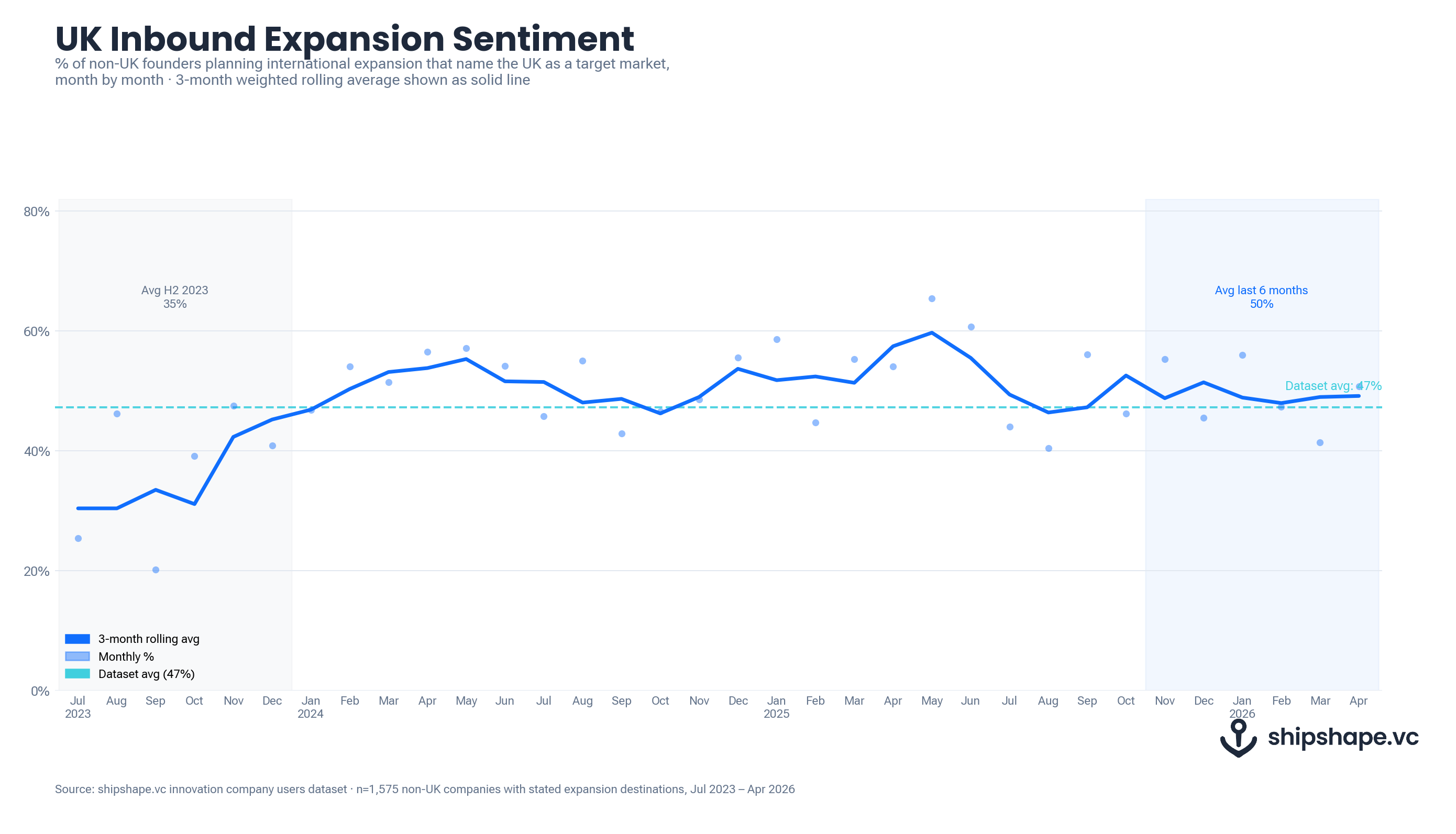

Nearly half of all non-UK founders planning international expansion name the United Kingdom as a target market.

That figure has held at close to forty-seven per cent across two years of data, through a change of government, a controversial Budgets, and persistent noise about the UK’s global competitiveness.

The chart above tracks, month by month, the share of non-UK founders on shipshape.vc who name the UK as an expansion destination, from July 2023 to April 2026.

The three-month weighted rolling average rarely dips below forty per cent or climbs above sixty. In a dataset that reflects founder intent in real time (updated as companies add or revise their expansion plans), the UK appears to have an enduring appeal to innovation companies overseas.

Where the data comes from

This piece draws on shipshape.vc’s innovation company users dataset. shipshape.vc is a free investment search engine that helps innovation companies access research on potential investors — Angels, Angel Syndicates, VC, CVC, and PE.

When a founder joins the platform, they can state which markets they are targeting for expansion; that stated intent is what we are measuring here.

The inbound analysis covers 1,028 non-UK companies with stated expansion destinations active between May 2024 and April 2026.

The UK founders’ analysis covers 1,289 UK-headquartered companies over the same window.

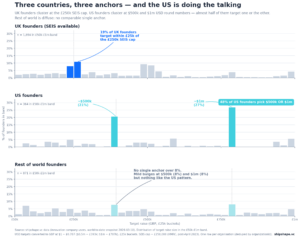

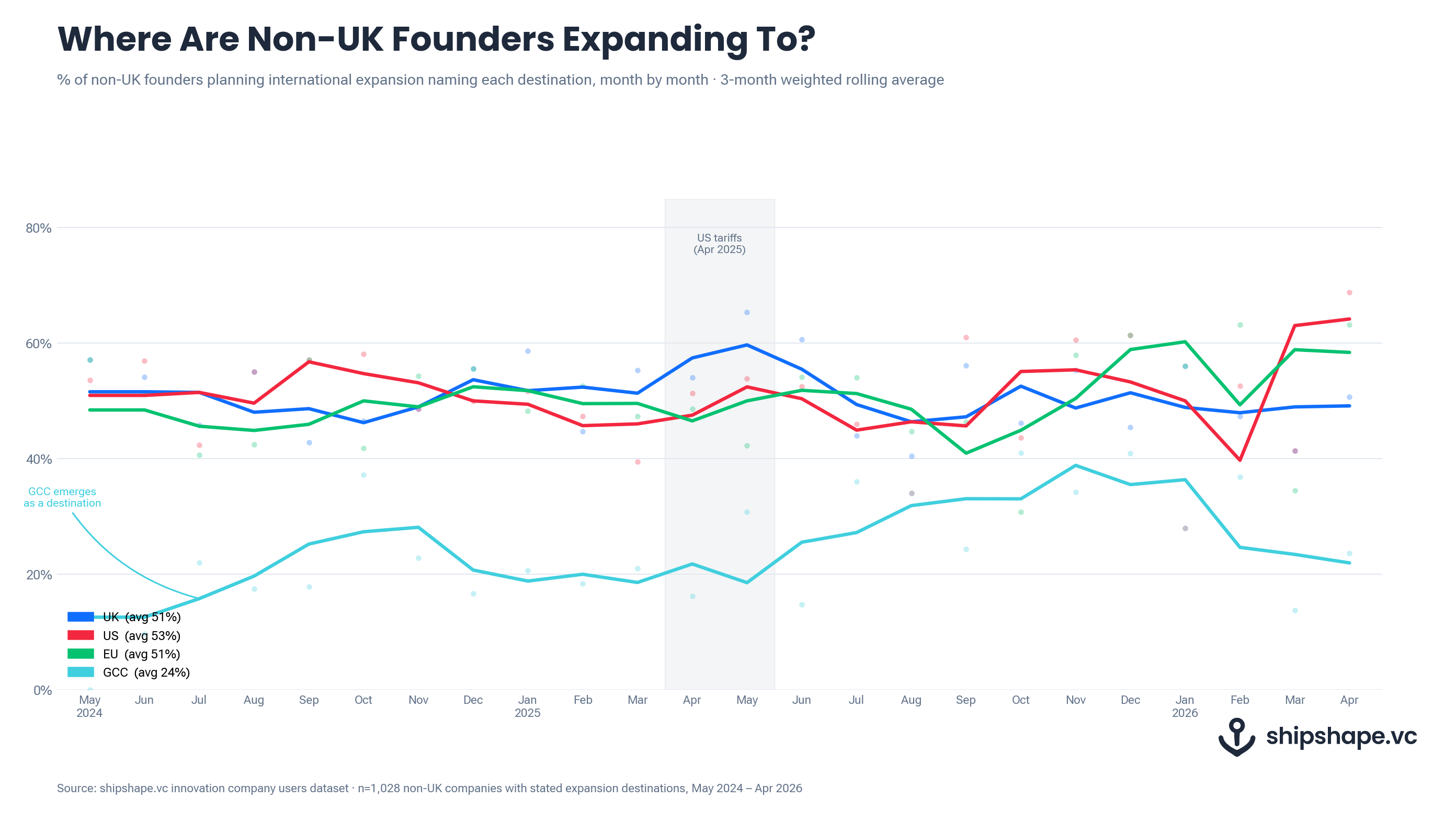

In the graph below, we track four destinations: the United States, the European Union, the United Kingdom, and the Gulf Cooperation Council (GCC).

Popular (for the moment) despite signficant upheaval

The period this data covers has not been a quiet one for the UK; A general election in July 2024 ended fourteen years of Conservative government and brought Labour in with a substantial majority.

The Autumn Budget of October 2024 raised employer National Insurance contributions and tightened the fiscal envelope in ways that generated considerable business commentary about the UK’s attractiveness as an investment destination.

There is no dip around the election, no dip around the Budget (though this did see UK founders increasingly look elsewhere), no response to any of the political events that dominated UK business news across this period.

The foreign founders in our dataset who are considering the UK as an expansion market are not (it seems) closely tracking the cycles of UK domestic political debate.

There are some core assets that it is hard for any Government to signficantly erode: language, legal system, time zone, density of talent (at a nominally low salary cost), and availability of capital in particular sectors.

That said, it is rarely a standalone destination, often forming part of a bundle of Western economy expansion destinations.

A ‘bundle’: UK, US and EU are often mentioned together

When you broaden the view to four major destinations, the United Kingdom, the United States and the European Union are named a similar proportion of founders and c-suites (averaging fifty-one to fifty-three per cent over the period).

A founder from India, Germany, the UAE or the United States who is building for global scale names all three (UK, US, EU) nearly as often as they name any one of them.

This has an important implication for how the UK should think about inbound competition, tt is not primarily competing with the US for the same pool of innovation companies.

The UK is competing — along with the US and the EU — for the attention and, more importantly, the follow-through of founders who have already decided to go West/cross the Atlantic.

We decided to include GCC also in the dataset due to the signficant effort and movement that Europe in particular has seen in terms of companies and skilled personnel moving to the region (UAE dominates).

The GCC starts the period at around twenty per cent, below the three Western anchors, and climbs steadily through 2025.

By October 2025 it is approaching forty per cent in some months — not yet at ‘Western’ levels, but no longer an afterthought.

There are a number of potential factors that have led to this: the visibility of Gulf VC, the UAE’s deliberate talent and capital visa strategy, and Saudi Arabia’s ambitions all became more obvious to a wider audience of founders.

The Iran conflict has also had a significant impact (as seen in Q1-Q2 2026).

Trump tarrifs

There is a moment in the UK inbound data that breaks from the trend: May 2025, when the UK share rises to sixty-five per cent, the highest reading we have recorded.

May 2025 comes six weeks after the United States announced sweeping tariffs on most trading partners — what was labelled ‘Liberation Day’, on 2 April 2025. But the more revealing number is the one immediately before the UK spike: in March 2025, the share of the same non-UK cohort naming the United States as an expansion target fell to thirty-nine per cent, the lowest US reading in the dataset. The US dip precedes the formal tariff announcement, which suggests founders were already repricing US expansion risk in the weeks before the announcement, perhaps in response to the building signals of trade policy shift that preceded it.

In April and May 2025, with US sentiment subdued, the UK-US gap runs at its widest in the period.

By Q3 2025 both normalise (The US recovers, and the UK settles back toward its long-run average).

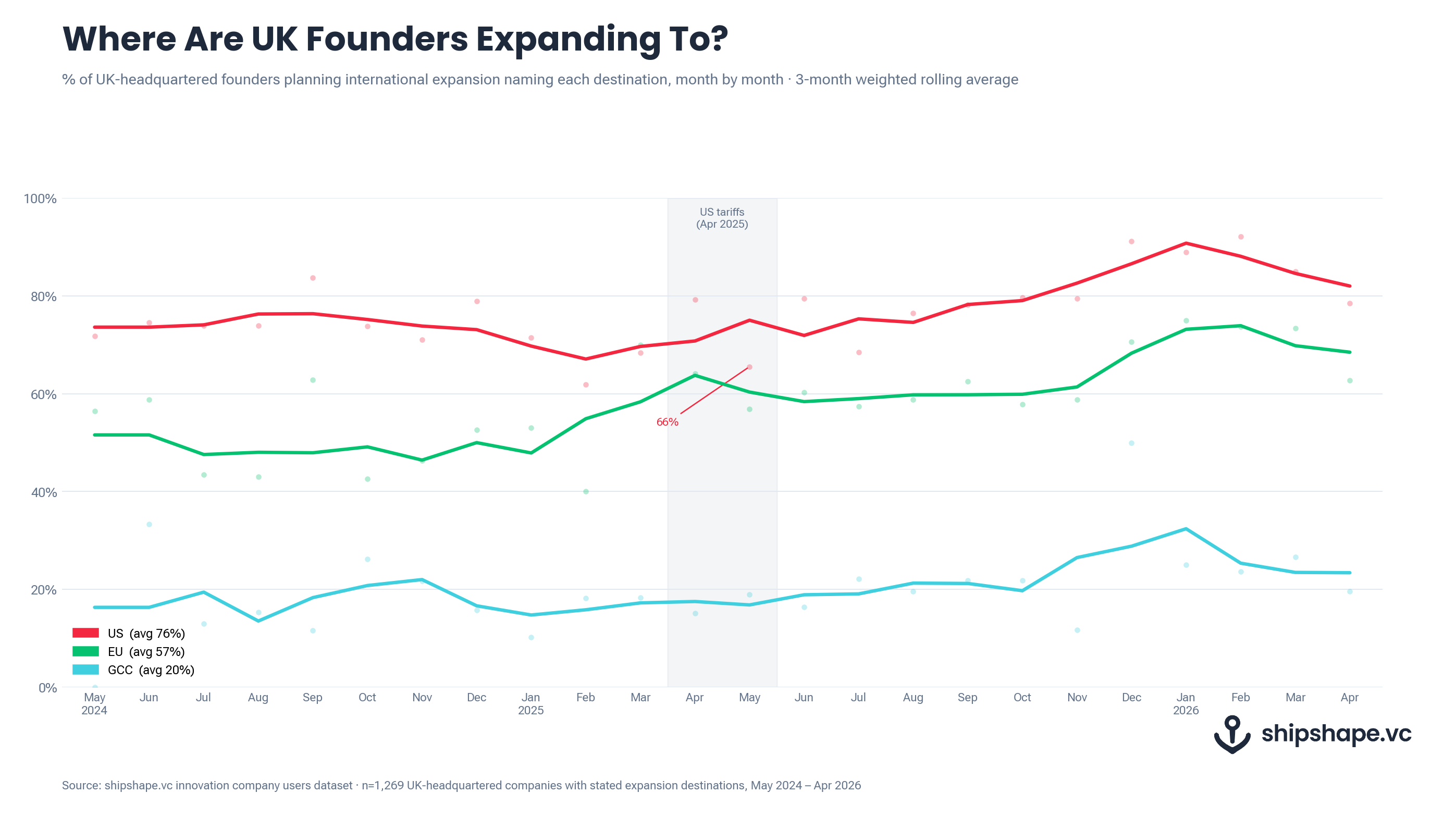

UK founders are hedging toward Europe

The tariff signal is visible on the other side of the ledger too, and it is more persistent.

For UK-headquartered founders, the United States is the dominant expansion destination, averaging seventy-six per cent, far ahead of any other market.

But around the tariff announcement window in April and May 2025, US intent among UK founders dips to sixty-six per cent, its lowest reading in the period, while EU intent simultaneously climbs and then continues rising through the second half of 2025, reaching the low seventies by late 2025 and early 2026.

Unlike the inbound rotation, which unwound within a quarter, the EU uptick has lasted longer.

The GCC sits at a steady average of twenty per cent among UK founders, lower than among the non-UK cohort but with a similar gradual upward trend through late 2025 and into 2026.

What the data does and does not show

These are stated intentions, not executed expansions. A founder who names the UK, the US and the EU as targets may follow through on one, two, or none of them. The dataset cannot distinguish between a company that has opened a London office and one that ticked a box when registering and never revisited it.

What it can show is which markets are being considered by an innovation company.

Source: shipshape.vc innovation company users dataset · inbound analysis: n=1,028 non-UK companies with stated expansion destinations, May 2024 – April 2026 · UK founders analysis: n=1,289 UK-headquartered companies, May 2024 – April 2026.

Tracking where the world’s founders plan to expand is one of the things we do with our innovation company users dataset. If you’re an investor, economic developer, or founder looking to understand inbound demand for a specific market, start your search at shipshape.vc — it’s free.