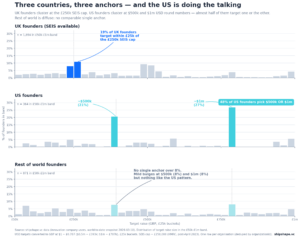

Seventy-three per cent of UK founders who name any international expansion destination name the United States, and twenty-two per cent name the US as their only destination — the only place they have flagged.

By contrast, when an American founder picks the UK, the UK is rarely the only place they pick: the median US founder eyeing Britain names four destinations in total, with the UK sitting alongside the EU, broader Europe, and almost always Canada or Latin America.

The asymmetry: UK as exporter, US as magnet

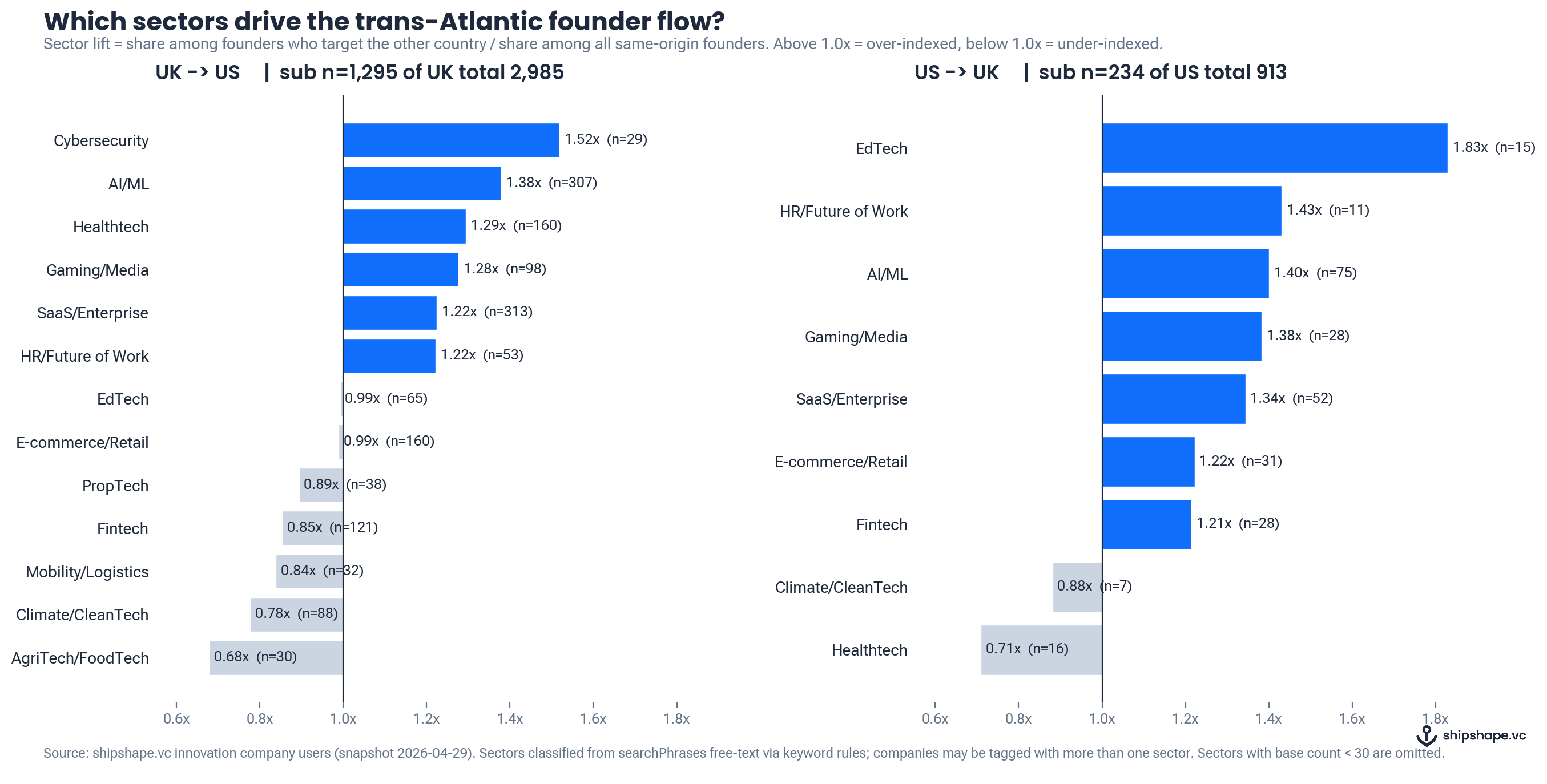

Of the 1,784 UK companies that have named any international expansion target, 1,295 (seventy-three per cent) name the United States.

The next destinations on the UK chart are the EU at forty-six per cent, the rest of Europe at twenty-five per cent, and the GCC at fourteen per cent. Nothing else comes close to the US share. For roughly one in five US-bound UK founders, no other country has been named at all — the US is the entire international plan.

By contrast, when an American founder picks the UK, the UK is rarely the only place they pick: the median US founder eyeing Britain names four destinations in total, with the UK sitting alongside the EU, broader Europe, and almost always Canada or Latin America. The two flows have the same direction of travel but very different psychology.

There are lessons in competition here for UK FDI teams (though most incentives are centralised in Whitehall, unlike the US, which has significant devolved State, County and local incentives to play with).

On the US side, of the 454 American companies that have named any expansion target, 234 (fifty-two per cent) name the United Kingdom. That is the largest single-country share on the US side and larger than the EU’s forty-eight per cent, larger than LatAm’s twenty-seven per cent, and larger than either Asian region.

But the UK rarely stands alone for these founders. Only nine per cent of US→UK founders name the UK as their sole destination, against twenty-two per cent of UK→US founders naming the US alone.

American founders heading to Britain are typically targeting Britain, the EU, the rest of Europe, and Canada — a spread that reads more like a checklist of Western markets than a focused bet on the United Kingdom.

Different sector preferences (notes to UK and US FDI teams)

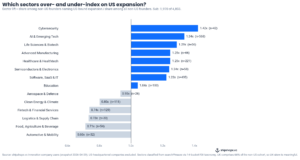

The two flows are not mirror images at the sector level either.

UK founders aiming at the US over-index (relative to the UK baseline) in cybersecurity (1.52×), AI/ML (1.38×), healthtech (1.29×), gaming and media (1.28×), and SaaS or enterprise software (1.22×).

They under-index in agritech and foodtech (0.68×), climate and clean tech (0.78×), mobility and logistics (0.84×), and a surprise on the list is fintech (0.85×).

UK fintech founders are slightly less likely to target the US than the average UK founder, which contradicts the usual story about the trans-Atlantic fintech corridor and is worth flagging versus common industry narratives.

US founders aiming at the UK over-index in different sectors: edtech (1.83× the US baseline), HR and future-of-work (1.43×), AI/ML (1.40×), gaming and media (1.38×), and SaaS / enterprise software (1.34×). The edtech lift is the biggest single sector skew in either direction — American edtech founders are nearly twice as likely as the average US founder in our dataset to name the UK as a target. A potential hypothesis is that the UK’s English-language schooling market with shared accreditation conventions and a tractable single buyer (state schools, the NHS, the civil service) is structurally easier to enter than the fifty-state patchwork at home, and edtech founders feel that edge more sharply than founders in sectors where regulatory differences cut the other way.

The two over-indexed lists overlap on AI/ML, gaming and media, and SaaS — these are the sectors in which the trans-Atlantic flow runs both ways.

Cybersecurity is uniquely a UK→US story; edtech and HR/future-of-work are uniquely a US→UK story.

Healthtech is interesting in being elevated for UK→US but depressed (0.71×) for US→UK.

UK healthtech companies potentially see the US as a market to crack; US healthtech does not see the UK that way (which is interesting given the observations for edtech and a smaller group of potential buyers in the UK vs. a myriad of US buyers in healthtech — though a far more lucrative potential market). Climate and clean tech are under-weighted in both directions, which possibly reflects different regulatory and Government attitudes.

Headlines for those attracting UK/US innovation companies

Sectors do matter in attractiveness, and there are misconceptions (e.g. about UK fintechs targeting expansion to the US) that do not seem to be reflected in our data.

AI/ML, gaming and media, and SaaS see strong two-way flows.

For US FDI teams, UK cybersecurity, AI/ML, healthtech, SaaS / enterprise SaaS, gaming and media innovation companies have a higher than average sentiment about US expansion.

For UK FDI teams, US edtechs are a good bet.

Where the data comes from

This piece is built on the international expansion intentions recorded by 2,985 UK-headquartered companies and 913 US-headquartered companies in shipshape.vc’s innovation-company users dataset, last updated on 29 April 2026.

We count a company as expansion-planning if it has named at least one destination the company intends to expand to in the next 18 months. Sector tags are derived from each company’s free-text searches via a keyword classifier; companies can be tagged with more than one sector.

All percentage lifts are computed against the relevant baseline, so “Cybersecurity 1.52×” means cybersecurity firms among UK→US-bound founders are 52 per cent over-represented relative to all UK firms in the dataset.

If you want to find out more about the underlying data — get in touch over LinkedIn or via daniel@shipshape.vc.