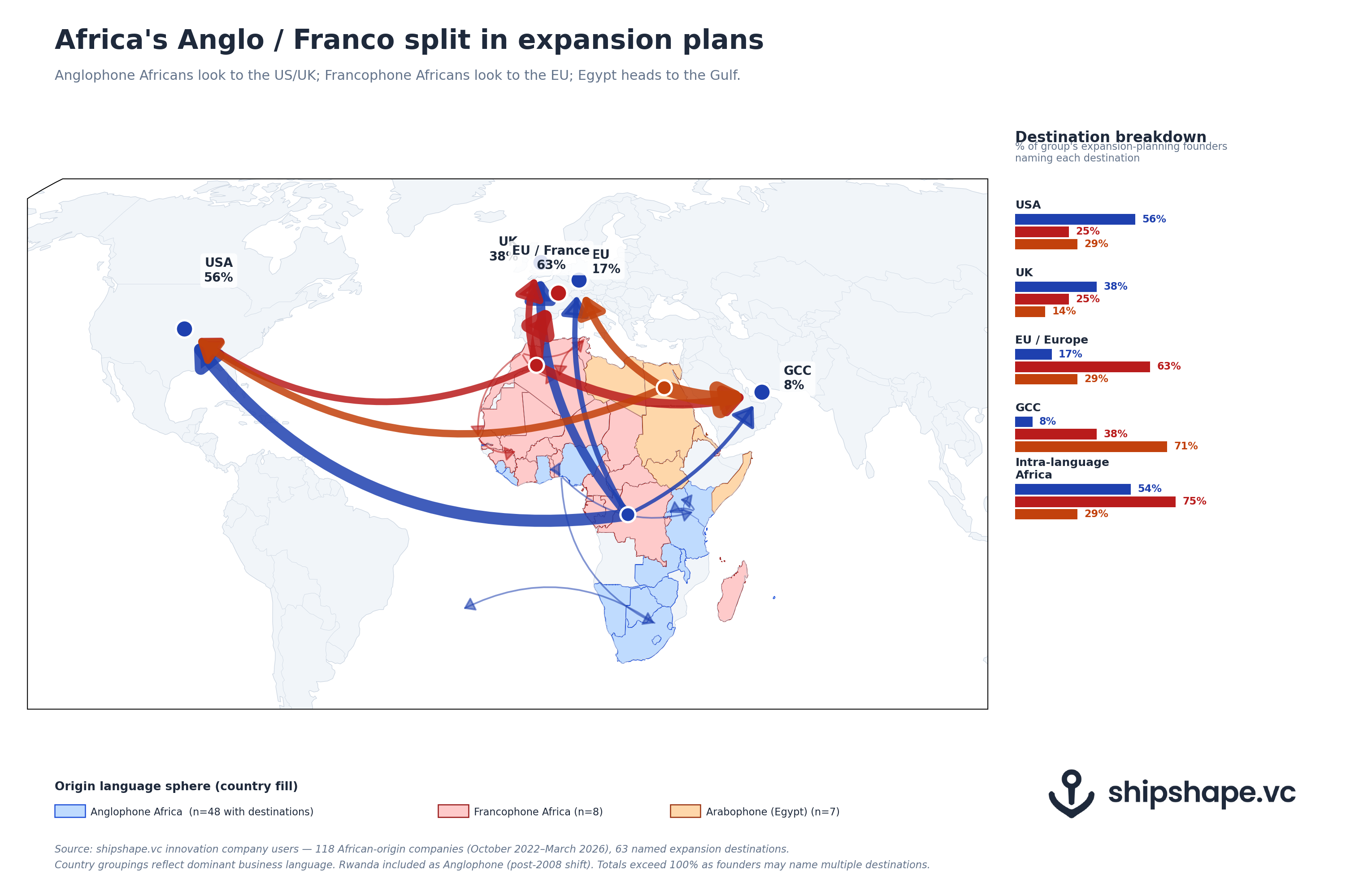

Anglophone African founders in our data plan to expand to the USA and the UK. Francophone African founders plan to expand to the EU and France. Egypt goes to the Gulf. And in every group, founders are most likely to expand within their own language sphere inside Africa before going further afield.

Please note this is based on a small sample size (n=118)

A note on sample size

Before reading too much into these numbers, the dataset is small. We have 118 African-origin companies in our innovation company users dataset between October 2022 and March 2026, of which 63 have named at least one international expansion destination. Within that, the Anglophone Africa cohort (n=48) is reasonable to draw observations from. The Francophone Africa cohort (n=8) and the Arabophone cohort (Egypt, n=7) are small enough that one or two founders move the percentages by ten to fifteen percentage points. We are sharing the chart because the patterns are consistent with cultural-ties theory and with our earlier diaspora analysis of larger origin markets; we would not yet treat the percentages as precise. Read this piece as a first signal, not a settled finding.

Where do we get our data?

This piece draws on the international expansion plans of African founders in our innovation company users dataset between October 2022 and March 2026. Origin countries are grouped by dominant business language: Anglophone (Nigeria, South Africa, Kenya, Ghana, Uganda, and others), Francophone (Morocco, Tunisia, Algeria, Senegal, Cameroon, Côte d’Ivoire, and others), and Arabophone (Egypt only at meaningful sample — Sudan, Libya, and Somalia are absent in our African-origin cohort at this volume). Rwanda is included as Anglophone, reflecting its post-2008 shift in business language. Founders may name more than one destination, so the percentages do not sum to 100.

Anglophone Africa goes to the Anglosphere

Of the 48 Anglophone African founders planning international expansion, 56% name the USA and 38% name the UK. The EU trails substantially at 17%. This is the diaspora hypothesis in its tightest form: where shared business language and deep migration history align with a destination, founders’ expansion plans follow. The USA pull is the stronger of the two, which is consistent with what our broader dataset tells us about how founders weight market size on top of language, but the UK figure is the highest UK score we see from any African origin.

There is a second finding sitting alongside the trans-Atlantic story, and arguably the more important one: 54% of Anglophone African founders name another Anglophone African country as an expansion destination. Anglophone African founders are first and foremost building for other Anglophone African markets, with the Anglosphere outside Africa as the next ring out.

Francophone Africa goes to France and the EU — directionally

The Francophone African cohort is small (n=8), so the headline numbers are directional rather than statistical. Within that caveat: 63% name the EU or France, 75% name another Francophone African country, 38% name the GCC, and 25% each name the USA and the UK. The shape mirrors the Anglophone pattern. The language sphere closest to home is the strongest pull, the dominant language outside Africa is the next, and English-speaking destinations are a secondary consideration. The 38% GCC figure (three founders out of eight) is the one we would most want a larger sample to confirm; it sits higher than the equivalent Anglophone GCC figure and would be worth understanding if it holds up.

Egypt’s Gulf orbit

Egyptian founders in our data (n=7) show the clearest single-destination story on the continent: 71% name the GCC, which is five founders out of seven. The cultural and linguistic ties to the Arabic-speaking Gulf are obvious. What is striking is how thin the secondary destinations are by comparison; the EU and USA are tied at 29% each, with little volume reaching the rest of Africa. The cohort is too small to do more than note the orbit, but the orbit is there.

What this adds to the diaspora picture

In our previous piece on diaspora patterns in expansion plans, we set out a hypothesis: linguistic and cultural ties give founders an unfair advantage in destination markets, and at the cohort level those advantages show up in where founders actually plan to expand. The African data, with all the sample-size caveats above, is consistent with that hypothesis. Anglophone Africans go to the Anglosphere. Francophone Africans go to the Francosphere. Egypt goes to the Arabic-speaking Gulf. Within Africa, founders cluster inside their own language sphere first.

The pattern would be more useful, and more rigorous, with more data. We will revisit this analysis when our African-origin cohort is materially larger; today’s chart is a first read, not a final word.

If you are a founder building from an African origin market and looking for investors who understand your target geographies, you can build your free fundraising profile and start your search at shipshape.vc. If you would like to read more analyses like this, you will find them on the shipshape.vc blog.

Sources: shipshape.vc innovation company users dataset (118 African-origin companies, 63 with named expansion destinations, October 2022 to March 2026). Country groupings reflect dominant business language. Rwanda included as Anglophone (post-2008 shift). Totals exceed 100% as founders may name multiple destinations.