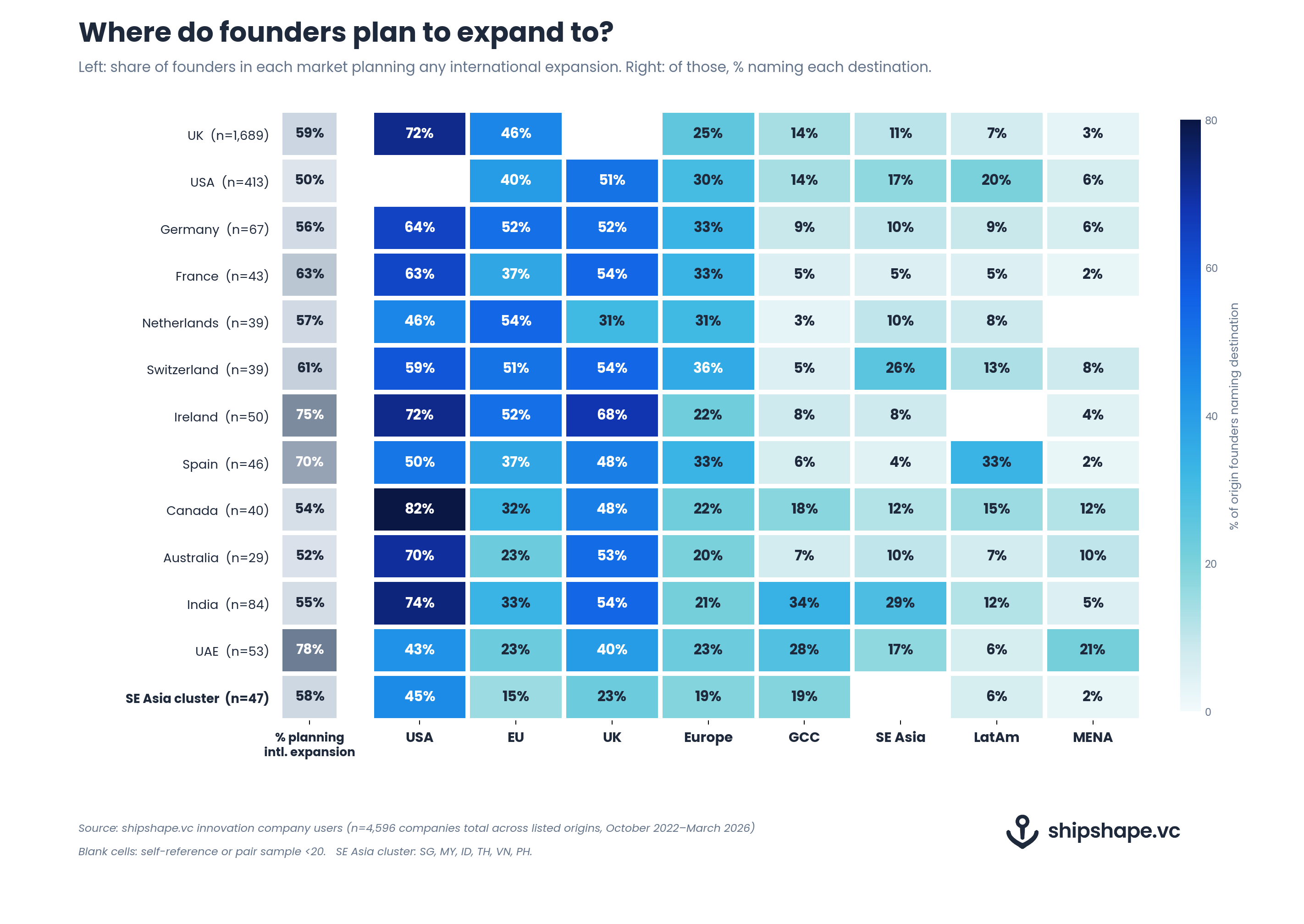

Sixty-eight per cent of Irish founders in our dataset who are planning international expansion name the UK as a destination market.

Thirty-four per cent of Indian founders name the GCC.

A third of Spanish founders name Latin America.

Each of these is the highest score for that destination across the entire chart, and the gap between these origin/destination pairs and the next-strongest scores is wider than market size would predict on its own.

A hypothesis is that linguistic and cultural ties give founders an unfair advantage / bias for entering a new market. Fluency in a customer’s language, cultural affinity, family or community presence on the ground all reduce the hurdles.

The patterns in our data line up with that hypothesis. A planned downstream project for us at shipshape.vc is a linguistic analysis of founder surnames against destination markets. For now, we are looking at the destinations themselves.

Where do we get our data?

This piece is built on the international expansion plans of 4,596 founders who have used shipshape.vc between October 2022 and March 2026, drawn from our innovation company users dataset.

We grouped origin markets where we had at least 29 founders planning international expansion; smaller cohorts are excluded because the percentages would then get noisy.

Destinations are bucketed by region (USA, EU ex-UK, UK, broader Europe, GCC, SE Asia, LatAm, MENA). Founders can name more than one market they intend to expand their company to.

The first column of the chart is the share of founders in each origin who plan any international expansion at all, which ranges from 44% to 78% across the markets we cover.

Irish companies target Britain

Sixty-eight per cent of Irish founders in our data who plan to expand internationally name the UK. No other origin in our dataset crosses 50% on the UK column. The Republic has a population of just over five million; the Irish-born population of England and Wales alone was 523,014 at the 2021 census, and the population with Irish heritage runs several times higher. Add a shared language, the Common Travel Area, and a long history of professional and family networks running across the Irish Sea, and Irish founders expanding into Britain start face fewer hurdles than an equivalent founder without these.

India’s Gulf weighting

Thirty-four per cent of Indian founders name the GCC and 29% name Southeast Asia, the two highest scores on either column for any origin we measure.

The GCC hosts around nine million Indian nationals, with roughly four million in the UAE alone, where Indians make up close to 40% of the resident population.

Singapore and Malaysia carry significant Indian-origin communities too. For an Indian founder building in fintech, healthcare, or consumer, the cultural and language fluency advantages in these markets are real, and the customers, distributors, and hires to make a launch land are already there.

Spain follows the language

Thirty-three per cent of Spanish founders in our data name Latin America. No other country of origin comes near that figure for Latin America. Spain has been the second-largest source of foreign direct investment into Latin America after the US for most of the last two decades, and 63% of Spanish companies surveyed by IE Business School plan to increase investment in the region in 2025. Three of the ten largest banks in Latin America are subsidiaries of Spanish parents. The shared language is the obvious factor; the durable corporate, banking, and migration links sitting on top of it are what turn cultural affinity into a default expansion path.

The UAE pulls regionally

Forty per cent of UAE-based founders name the UK, 28% name the GCC, and 21% name MENA. The UAE pattern is not strictly diaspora in the same sense as the others. Only around 11% of the UAE population are Emirati nationals, and many of the founders in our dataset are themselves part of the country’s expatriate communities. What we are measuring here is closer to regional gravity: Dubai and Abu Dhabi function as the practical hub for Arabic-language and MENA-facing businesses, and the founders building from there expand into the markets they are already operating across. The UK column reflects the long-running UAE-UK corporate, education, and family corridor. Beyond the diaspora pattern, the UAE has deliberately pursued stronger international ties through trade agreements, free zones, and talent and capital visas, and our expansion data reflects that strategy.

A few quieter signals

Some smaller patterns sit alongside the headline ones. Australian founders name the UK at 53%, the second-highest UK score in our dataset, consistent with the deep British-Australian corporate and migration ties. Canadian founders name the USA at 82%, the most concentrated single-destination figure in the chart, where geographic proximity, language, and cross-border family and business networks all point the same way. Switzerland’s 26% naming Southeast Asia is harder to explain through diaspora alone and looks like a sector effect rather than a network one. The drivers behind Southeast Asia’s attraction for Swiss companies will be worth exploring in greater detail in a future piece.

What this changes

Cultural and linguistic ties have a strong bearing on the attractiveness of new markets to founders. Our data does not say that founders ignore market size; it says that, alongside size, founders weight the markets where they hold unfair advantages, and at the cohort level those advantages are visible in expansion plans. For investors backing companies with international ambition, it is worth asking which markets a team has unfair advantages in, not just which markets they say they are targeting. The answer is frequently already there in the languages founders grew up with, the diasporas they belong to, or the regions where they have spent their working lives.

We will keep monitoring how these patterns shift as our dataset grows.

If you are a founder planning international expansion, you can build your free fundraisi